The fact that the vast majority of the American general public believe that the US economy is still in recession. According to a CNN poll (see here) only 18% of Americans believe that we are not in recession right now, so this also does not accord with the way that economists measure recessions, and suggests that we might need to review this, or at least re-categorise the phases of the business cycle!

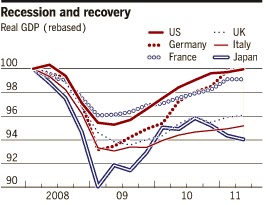

So what should be our measure of a "recession"? I have heard many commentators say that although we are still not officially in a recession, it sure still feels like one, particularly when unemployment is still high and there are still calls for economic stimulus like the one heard only today from Fed Chicago District President Charles Evans (see here). But given what has happened in Japan and what appears to be happening in some other developed countries, maybe we should reconsider our definition of recession as a cyclical downturn and recovery up to the point where we surpass the level of real GDP achieved at the peak of the previous boom. In fact with a growing population even this is unsatisfactory because 4 years ago in 2007 the population was smaller than it is today in nearly all of these countries ( - the exception perhaps being Japan) so if we measure output on the basis of output per head of population (or per capita), we would take longer than indicated in the graph above to get to the same level of output per capita so we would be calling the recession over before it really ended. In fact, to be frank I am in favor of changing our definition of a recession because the current measure only focuses on the downturn and does not focus on what happens afterwards - plainly Japan's experience in the 1990s plus our own recent experience suggest that not all downturns are followed by rapid upturns.

I think a much more serious problem is another quite different story that the New York Times (august newspaper though it is) does not bring out in its reporting. If you look at the recessions of the 1970s, 80s and 90s and then the 2 recessions of the 00s, it seems clear to me that the US labor market is much less able to cope with recessions than it used to be - the recovery times seem to be longer and much more drawn out than they were even 20 years ago. To me this implies that there is some very serious changes going on - some of it structural, but I think something must be also be going on in terms of reluctance to hire - for example do companies delay hiring much longer than they used to, asking their current employees to do more overtime for a longer period of time before they decide to bite the bullet? I'm not sure we know the answers to these questions yet, but clearly things are changing for US workers, and changing fast! A pretty grim interpretation for the reasons for this are also given today by Robert Reich in the New York Times and although I don't go along with everything he says, I do agree that we need to focus on education, but I would also add that the US really also needs to focus on marketing itself to the rest of the world - countries that sell products to the developing countries (where the economic growth is right now) is one of the best ways to help expand our economy.

So to answer the question I pose for this blog, the response is clearly a resounding "No"! But for all the problems with the labor market ( - and given that it's really no surprise that Obama recently chose a Labor economist, Alan B. Krueger, to head up his economic team), the US has a lot going for it. It has some of the most dynamic companies in the world, and it is far ahead of most countries in the area of technology - but these advantages will narrow compared to Europe and Asia if the US does not focus on what leads to these advantages - education! I think what the US is essentially finding out is that although the military gave you economic power back during the cold war, spending a lot on military does not give you that advantage now. Countries that have focused more on education over the last 20 years (e.g. Finland, Germany, South Korea etc) are now doing very well thank you - countries that have not grown as fast.

What should be done then? I think a good start would be to redefine what a recession is, re-prioritize government spending towards education and away from the military, and to set up some kind of corporate international opportunities bureau which would list foreign opportunities and so US companies would be more aware and able to more easily grasp new overseas opportunities.