In an attempt to respond to the requests for my views on what is going on with the US macroeconomy in particular right now, but also in general for the world economy, I have decided to come out of enforced hibernation and put fingertip to keyboard. We certainly live in interesting times, and although we were definitely due a recession, as usual the source of the recession was somewhat of a surprise.

To preview what the basic message is in this blog posting, if anyone is in any doubt that a global recession is occurring, I think you have to study the rather disconcerting facts about the economic impact of both OPEC and this virus, and then even without any statistics it becomes quite obvious that for both the US and UK, and many other parts of the world, a deep recession is now underway. Quite why the US Treasury Secretary, Steven Mnuchin (see here), thought that the US would avoid a recession, is beyond me. Some think his forecast was made to keep up morale, but I think that in fact it undermines the credibility of the position of the Treasury Secretary. I would also note here that soon afterwards, the Treasury Secretary appears to have reversed his views, noting that the US economy could very soon experience an unemployment rate of 20%.

In this blog post, therefore, I want to review what I think could be the economic impacts, and then give my take on what should be done from an economic perspective.

Before we start though, let's get some definitional things sorted out. First, this is a real "shock" in the proper sense of the word. Economists use this word "shock" to mean any development or change in conditions that impacts the economy, but it is usually from some kind of change in human behavior or asset bubble. To be honest I don't think of these changes as "shocks" per se, as they are not really sudden changes that are impacting the economic system, but are rather what I would call a "development" or change in the economic environment. The OPEC change in policy with regards to oil quotas is a good example of this - there is a change in one sector which ricochets through the economy. The corona virus, however, is not like just a change in the behavior of certain market participants or an industry with knock on effects; this is a real "shock" in the sense of a wholesale change in economic circumstances with everyone having to adapt to a sudden new environment, with some sectors of the economy closing down entirely, and others seeing booming conditions.

Secondly, the question as to whether this is a supply shock or a demand shock - our macroeconomics is really inadequate in describing what is going on right now, as clearly we have both supply and demand side effects happening, so although I see economists arguing that this is a supply shock rather than a demand shock, this distinction is irrelevant as what we have is a contractionary economic event, both on the supply and demand sides of the economy. And this also means that the usual textbook monetary policy channel responses are unlikely to help much in stimulating the economy, as both investment and consumer spending is really not dependent on interest rates, and spending opportunities are now quite limited.

Next we need to think about the steps with which this recession is being brought on, and in my own opinion how it might play out. So first the corona virus rears it's ugly head in China and causes supply problems for US firms due to the fallout in the Chinese economy - oh and incidentally the Chinese economic numbers released last night ( - see here) showed factory output falling by 13.5% during January and February compared with the previous year. And in addition to statistics on factory output the retail sales figures were down 20% and investment figures were down 25% compared with a year ago. Now remember here too, that China, as it is a communist country, had a centralized response to the virus, and only locked down one Chinese province (Hubei Province), and so contained the spread. So just imagine if the virus had caused a complete lockdown of the entire country - and yes, that means that these figures would have been even worse. Indeed although the Chinese claim to be over the virus and almost fully recovered, this seems quite suspicious to me, and I understand from my contacts in that country that there are still cases arising, but everyone now takes appropriate precautions.

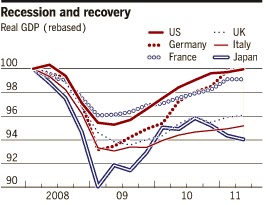

The virus has spread to Europe next, with whole countries on lockdown, with whole swathes of their economies' ground to a halt. That will surely mean even steeper falls in output in countries like Italy and now France and Germany. The virus is now definitely spreading in North America too, and that has caused some draconian measures which (as it is now doing in Europe) will cause a collapse in output in certain industries ( - think cruises, tourism and the travel industry, consumer discretionary spending, entertainment and the housing industry).

The virus has spread to Europe next, with whole countries on lockdown, with whole swathes of their economies' ground to a halt. That will surely mean even steeper falls in output in countries like Italy and now France and Germany. The virus is now definitely spreading in North America too, and that has caused some draconian measures which (as it is now doing in Europe) will cause a collapse in output in certain industries ( - think cruises, tourism and the travel industry, consumer discretionary spending, entertainment and the housing industry).

The second catalyst for recession in the case of the US is the collapse of the OPEC meeting on March 8th (see here), which caused Saudi Arabia to increase output massively, prompting oil prices to collapse to roughly half of where they were before the OPEC meeting. This collapse in oil prices, while being good for consumers ( - the US President referred to it as having the same effect as a tax cut), is a real blow to the US fracking industry if these low oil prices persist for any period of time. Why is this? Well most fracking wells are not profitable at prices below roughly $40 a barrel, so with prices now down at $22.63, nearly all of the US fracking oil companies will be losing money. What's more, many of them had bought substantial tracts of land in the heady days when oil was over $100 a barrel, and had borrowed heavily to do so. So many of these companies are heavily indebted and are unlikely to be able to survive long at these current oil prices - in fact recent reports show that they are already laying off thousands of workers (see here).

So what is happening now with the spread of the virus in North America is that the workers in the oil, transportation, entertainment, tourism and consumer discretionary are being laid off, and hence unemployment is undoubtedly rising, and probably much faster than we realize. In most locations in the US all bars, clubs, cinemas and restaurants are closed, and in other cities measures are even more draconian.

To gauge the percentage of US GDP that we are talking about here, let us look at US output by sector for 2018 ( - this still hasn't been completed for 2019). For all industries we saw an increase of 6.1% in 2018 over 2017, but of course this is in nominal amounts, so adjusting for inflation, we have to subtract inflation which in 2018 was about 2.3%, which gives us a real output increase of roughly 3.8%, which is obviously a little higher than the 3% real GDP estimate from the BEA due to the fact that GDP subtracts out the items that are intermediate goods ( - goods which are used in the production of something else).

So running down this table we can see that the industries that are at risk are on lines 4, 11, 12, 16 and 24. Now let's make some back of the envelope assumptions and say that we have a similar situation as in 2018 in terms of output amounts. Let's also assume that we are looking at the first quarter of 2020, so we are only talking about one month out of the whole quarter being subject to this shock. So let's do some very rough and approximate calculations for the last month (March).

First, mining (which is mostly oil and gas) gets cut in half (-$250m in 2018), retail trade slows by about 25% (-$465.73), transportation and warehousing falls by 25% (-$316.50m), real estate also takes a hit of around 25% (-$1000m) and lastly arts and entertainment and accommodation get cut in half (-$750m). Note that this does not include any multiplier effects or "knock-on" effects (to other industries) and nor does it include the likely increase in the output of the healthcare sector due to hospital stays.

So when looking at the change in output from 2017 to 2018 this went up by 6.01% in nominal terms. Now if we take off the conservative estimates of the fall in output that would have occurred if the Corona virus had hit the US during that year, we get $2,781m which when subtracted from the 2018 total would give us $33,812.3. But recall in the first quarter that only the month of March would likely see this fall, so then that gives us about a fall of around $930m. When you do the calculations as to the nominal growth rate you get about 3.4% which when adjusted for inflation comes out to be roughly 1%, but then taking out the intermediate goods this will bring us down to roughly a stagnant economy with real growth of around 0% in the first quarter. So my forecast for GDP growth in Q1 is 0% or somewhere close to this.

The 2nd quarter will likely be much worse than the 1st quarter though, and while I don't wish to speculate how bad it will be ( - Goldman Sachs already is forecasting a 24% fall in real GDP), it will definitely put us in recession territory given that it goes on beyond 2 weeks. But once again let's do a "back of the envelope" extremely rough calculation. One of the reasons I did not include the multiplier effects for Q1 is that they take time to filter through. If we assume that this corona virus and OPEC situation persists for the whole of Q2 and that we have a 1.4 multiplier effect on the fall in output then we get approximately $4,000m which then make our change in nominal output -5.5%, but then taking off the inflation rate to get a real rate of growth we end up with -8%, which then taking off roughly another 1% to adjust for intermediate goods gets us to roughly a -10% year over year growth rate. I would also add that this is also a conservative estimate as it assumes no "knock on" effects so only a limited impact on the sectors of the economy not accounted for above.

Exactly what might be the impact on unemployment of this fall in real GDP growth? Just to illustrate, according to Okun's law (which is the relationship between unemployment and economic growth, if we see economic growth fall by a total of 13% (the difference between 3% (for last year) and an estimate of Q2 growth of say -10%, that means that (if Okun's law prevails) the unemployment rate would increase by 6.5% from its current level of around 3.5% to 10%, which is the level it reached during the great recession.

Obviously you can do further math which could show things deteriorating much further, but I think you get the picture - at the minimum we are looking at a really sharp recession that, macroeconomically speaking, is at least as bad as the "great recession" of 2008 to 2009, with the likelihood that it could be much worse if this worsens throughout Q2. Of course if things improve and the viral spread is brought under control quickly as it appears to have been the case in China, then these scenarios brighten considerably.

Now let's look at the policy responses.

On the monetary side, the Fed has been busy pumping money into the economy by resurrecting some of the tools that it used during the "great recession". These are summed up here, and they should have the desired effect of safeguarding solvent financial institutions from the negative impact of the corona virus and the fallout from the latest OPEC meeting. This is important as it provides for lines of credit by financial institutions (such as banks) to their clients, and makes sure that the banks have virtually unlimited funding (from the Fed) to supply this assistance. Obviously this applies to solvent companies, as even with unlimited backing, few banks are going to want to provide credit to technically insolvent companies.

Given that both the OPEC and corona virus impacts are not really financial in nature though, but rather are a matter of providing funds to provide a social safety net and to assist industries that are heavily impacted, the burden of response must fall on fiscal policy. So, on the fiscal side, it is clear that both individuals that are impacted need assistance, and also industries that are impacted might also need and request some kind of government support. As of writing, the proposals coming out of Congress are essentially "helicopter money", with checks for households, and loans and grants to various industries. But what is apparent to me is that the government has not seemed to grasp the impact of the quarantining and closing up of businesses that necessitate social interaction, not only on the workers, but also on the firms within the industries. At the same time, it does seem to me to be incumbent upon the government to learn lessons both from previous recessions and from, for example, the Japanese experience with deflation. I understand that it is extremely difficult to design a fiscal stimulus package that will address an evolving situation, and obviously anything that Congress passes and which the President signs may have to be tweaked later. Nevertheless it seems to me that fiscal policy should:

a) provide immediate relief to those suffering hardship from being laid off or from lack of business if self-employed; and

b) provide support for industries that are incapacitated or have severe falloff in customers due to social distancing.

Although the current thinking for a) is that unemployment insurance and 2 checks, proposed by the current Treasury Secretary should be the first step, this is perhaps not the best way to provide assistance, as certainly the checks will not be targeted and will just be presumably to all taxpayers, regardless of income or job security. Plus one of the problems in just writing a check to citizens is that presumably a secondary important reason for doing so is to stimulate the macroeconomy. I would suggest that probably a better way of doing this is to provide a debit card to all citizens which would also have an expiration date - that way there would be more certainty that the money is injected into the economy through new spending. This money could be paid back through paying higher taxes for up to 5 years. Of course some individuals might still claim a debit card only to substitute that debit card spending for their own spending, but I would suggest that this is a better way than just giving individuals a check.

As for support for industries, I would not favor grants, which are one of the current preferred methods of support by the administration. I would favor small companies receiving loans with low interest rates, and larger companies that are in financial trouble having the ability to issue shares which the government would then purchase (as a secondary issuance). The cash that companies raise from selling partial ownership to the government would not be permitted to be spent on either share purchases from private citizens or on dividends or increased remuneration of management. The idea here is to give support where needed, but at the same time for the taxpayers money to be used in ways such that there is a return on the investment that the government makes in these struggling companies. And these facilities should not carry a fixed sum, but rather, should be a facility that any company in trouble can tap if required. Of course some of these companies will fail, but at least the government would not be supporting one industry at the expense of another, and would also have a broad portfolio of loans and shares which if properly diversified should yield a decent return for the taxpayer and not end up costing the government a dime.

As Winston Churchill once said: "Never let a good crisis go to waste" and what I fear right now is that our policymakers just do not seem to have the imagination to come up with some new ways of thinking about how to support the macroeconomy without increasing the national debt by an extremely large amount in the long run.

To preview what the basic message is in this blog posting, if anyone is in any doubt that a global recession is occurring, I think you have to study the rather disconcerting facts about the economic impact of both OPEC and this virus, and then even without any statistics it becomes quite obvious that for both the US and UK, and many other parts of the world, a deep recession is now underway. Quite why the US Treasury Secretary, Steven Mnuchin (see here), thought that the US would avoid a recession, is beyond me. Some think his forecast was made to keep up morale, but I think that in fact it undermines the credibility of the position of the Treasury Secretary. I would also note here that soon afterwards, the Treasury Secretary appears to have reversed his views, noting that the US economy could very soon experience an unemployment rate of 20%.

|

| The Corona virus along side human cells |

Secondly, the question as to whether this is a supply shock or a demand shock - our macroeconomics is really inadequate in describing what is going on right now, as clearly we have both supply and demand side effects happening, so although I see economists arguing that this is a supply shock rather than a demand shock, this distinction is irrelevant as what we have is a contractionary economic event, both on the supply and demand sides of the economy. And this also means that the usual textbook monetary policy channel responses are unlikely to help much in stimulating the economy, as both investment and consumer spending is really not dependent on interest rates, and spending opportunities are now quite limited.

Next we need to think about the steps with which this recession is being brought on, and in my own opinion how it might play out. So first the corona virus rears it's ugly head in China and causes supply problems for US firms due to the fallout in the Chinese economy - oh and incidentally the Chinese economic numbers released last night ( - see here) showed factory output falling by 13.5% during January and February compared with the previous year. And in addition to statistics on factory output the retail sales figures were down 20% and investment figures were down 25% compared with a year ago. Now remember here too, that China, as it is a communist country, had a centralized response to the virus, and only locked down one Chinese province (Hubei Province), and so contained the spread. So just imagine if the virus had caused a complete lockdown of the entire country - and yes, that means that these figures would have been even worse. Indeed although the Chinese claim to be over the virus and almost fully recovered, this seems quite suspicious to me, and I understand from my contacts in that country that there are still cases arising, but everyone now takes appropriate precautions.

The virus has spread to Europe next, with whole countries on lockdown, with whole swathes of their economies' ground to a halt. That will surely mean even steeper falls in output in countries like Italy and now France and Germany. The virus is now definitely spreading in North America too, and that has caused some draconian measures which (as it is now doing in Europe) will cause a collapse in output in certain industries ( - think cruises, tourism and the travel industry, consumer discretionary spending, entertainment and the housing industry).

The virus has spread to Europe next, with whole countries on lockdown, with whole swathes of their economies' ground to a halt. That will surely mean even steeper falls in output in countries like Italy and now France and Germany. The virus is now definitely spreading in North America too, and that has caused some draconian measures which (as it is now doing in Europe) will cause a collapse in output in certain industries ( - think cruises, tourism and the travel industry, consumer discretionary spending, entertainment and the housing industry). The second catalyst for recession in the case of the US is the collapse of the OPEC meeting on March 8th (see here), which caused Saudi Arabia to increase output massively, prompting oil prices to collapse to roughly half of where they were before the OPEC meeting. This collapse in oil prices, while being good for consumers ( - the US President referred to it as having the same effect as a tax cut), is a real blow to the US fracking industry if these low oil prices persist for any period of time. Why is this? Well most fracking wells are not profitable at prices below roughly $40 a barrel, so with prices now down at $22.63, nearly all of the US fracking oil companies will be losing money. What's more, many of them had bought substantial tracts of land in the heady days when oil was over $100 a barrel, and had borrowed heavily to do so. So many of these companies are heavily indebted and are unlikely to be able to survive long at these current oil prices - in fact recent reports show that they are already laying off thousands of workers (see here).

|

| The Corona Virus exiting a human cell |

To gauge the percentage of US GDP that we are talking about here, let us look at US output by sector for 2018 ( - this still hasn't been completed for 2019). For all industries we saw an increase of 6.1% in 2018 over 2017, but of course this is in nominal amounts, so adjusting for inflation, we have to subtract inflation which in 2018 was about 2.3%, which gives us a real output increase of roughly 3.8%, which is obviously a little higher than the 3% real GDP estimate from the BEA due to the fact that GDP subtracts out the items that are intermediate goods ( - goods which are used in the production of something else).

So running down this table we can see that the industries that are at risk are on lines 4, 11, 12, 16 and 24. Now let's make some back of the envelope assumptions and say that we have a similar situation as in 2018 in terms of output amounts. Let's also assume that we are looking at the first quarter of 2020, so we are only talking about one month out of the whole quarter being subject to this shock. So let's do some very rough and approximate calculations for the last month (March).

First, mining (which is mostly oil and gas) gets cut in half (-$250m in 2018), retail trade slows by about 25% (-$465.73), transportation and warehousing falls by 25% (-$316.50m), real estate also takes a hit of around 25% (-$1000m) and lastly arts and entertainment and accommodation get cut in half (-$750m). Note that this does not include any multiplier effects or "knock-on" effects (to other industries) and nor does it include the likely increase in the output of the healthcare sector due to hospital stays.

|

| https://www.bea.gov/system/files/2020-01/gdpind319.pdf Table 8 |

So when looking at the change in output from 2017 to 2018 this went up by 6.01% in nominal terms. Now if we take off the conservative estimates of the fall in output that would have occurred if the Corona virus had hit the US during that year, we get $2,781m which when subtracted from the 2018 total would give us $33,812.3. But recall in the first quarter that only the month of March would likely see this fall, so then that gives us about a fall of around $930m. When you do the calculations as to the nominal growth rate you get about 3.4% which when adjusted for inflation comes out to be roughly 1%, but then taking out the intermediate goods this will bring us down to roughly a stagnant economy with real growth of around 0% in the first quarter. So my forecast for GDP growth in Q1 is 0% or somewhere close to this.

The 2nd quarter will likely be much worse than the 1st quarter though, and while I don't wish to speculate how bad it will be ( - Goldman Sachs already is forecasting a 24% fall in real GDP), it will definitely put us in recession territory given that it goes on beyond 2 weeks. But once again let's do a "back of the envelope" extremely rough calculation. One of the reasons I did not include the multiplier effects for Q1 is that they take time to filter through. If we assume that this corona virus and OPEC situation persists for the whole of Q2 and that we have a 1.4 multiplier effect on the fall in output then we get approximately $4,000m which then make our change in nominal output -5.5%, but then taking off the inflation rate to get a real rate of growth we end up with -8%, which then taking off roughly another 1% to adjust for intermediate goods gets us to roughly a -10% year over year growth rate. I would also add that this is also a conservative estimate as it assumes no "knock on" effects so only a limited impact on the sectors of the economy not accounted for above.

Exactly what might be the impact on unemployment of this fall in real GDP growth? Just to illustrate, according to Okun's law (which is the relationship between unemployment and economic growth, if we see economic growth fall by a total of 13% (the difference between 3% (for last year) and an estimate of Q2 growth of say -10%, that means that (if Okun's law prevails) the unemployment rate would increase by 6.5% from its current level of around 3.5% to 10%, which is the level it reached during the great recession.

Obviously you can do further math which could show things deteriorating much further, but I think you get the picture - at the minimum we are looking at a really sharp recession that, macroeconomically speaking, is at least as bad as the "great recession" of 2008 to 2009, with the likelihood that it could be much worse if this worsens throughout Q2. Of course if things improve and the viral spread is brought under control quickly as it appears to have been the case in China, then these scenarios brighten considerably.

Now let's look at the policy responses.

On the monetary side, the Fed has been busy pumping money into the economy by resurrecting some of the tools that it used during the "great recession". These are summed up here, and they should have the desired effect of safeguarding solvent financial institutions from the negative impact of the corona virus and the fallout from the latest OPEC meeting. This is important as it provides for lines of credit by financial institutions (such as banks) to their clients, and makes sure that the banks have virtually unlimited funding (from the Fed) to supply this assistance. Obviously this applies to solvent companies, as even with unlimited backing, few banks are going to want to provide credit to technically insolvent companies.

Given that both the OPEC and corona virus impacts are not really financial in nature though, but rather are a matter of providing funds to provide a social safety net and to assist industries that are heavily impacted, the burden of response must fall on fiscal policy. So, on the fiscal side, it is clear that both individuals that are impacted need assistance, and also industries that are impacted might also need and request some kind of government support. As of writing, the proposals coming out of Congress are essentially "helicopter money", with checks for households, and loans and grants to various industries. But what is apparent to me is that the government has not seemed to grasp the impact of the quarantining and closing up of businesses that necessitate social interaction, not only on the workers, but also on the firms within the industries. At the same time, it does seem to me to be incumbent upon the government to learn lessons both from previous recessions and from, for example, the Japanese experience with deflation. I understand that it is extremely difficult to design a fiscal stimulus package that will address an evolving situation, and obviously anything that Congress passes and which the President signs may have to be tweaked later. Nevertheless it seems to me that fiscal policy should:

a) provide immediate relief to those suffering hardship from being laid off or from lack of business if self-employed; and

b) provide support for industries that are incapacitated or have severe falloff in customers due to social distancing.

Although the current thinking for a) is that unemployment insurance and 2 checks, proposed by the current Treasury Secretary should be the first step, this is perhaps not the best way to provide assistance, as certainly the checks will not be targeted and will just be presumably to all taxpayers, regardless of income or job security. Plus one of the problems in just writing a check to citizens is that presumably a secondary important reason for doing so is to stimulate the macroeconomy. I would suggest that probably a better way of doing this is to provide a debit card to all citizens which would also have an expiration date - that way there would be more certainty that the money is injected into the economy through new spending. This money could be paid back through paying higher taxes for up to 5 years. Of course some individuals might still claim a debit card only to substitute that debit card spending for their own spending, but I would suggest that this is a better way than just giving individuals a check.

As for support for industries, I would not favor grants, which are one of the current preferred methods of support by the administration. I would favor small companies receiving loans with low interest rates, and larger companies that are in financial trouble having the ability to issue shares which the government would then purchase (as a secondary issuance). The cash that companies raise from selling partial ownership to the government would not be permitted to be spent on either share purchases from private citizens or on dividends or increased remuneration of management. The idea here is to give support where needed, but at the same time for the taxpayers money to be used in ways such that there is a return on the investment that the government makes in these struggling companies. And these facilities should not carry a fixed sum, but rather, should be a facility that any company in trouble can tap if required. Of course some of these companies will fail, but at least the government would not be supporting one industry at the expense of another, and would also have a broad portfolio of loans and shares which if properly diversified should yield a decent return for the taxpayer and not end up costing the government a dime.

As Winston Churchill once said: "Never let a good crisis go to waste" and what I fear right now is that our policymakers just do not seem to have the imagination to come up with some new ways of thinking about how to support the macroeconomy without increasing the national debt by an extremely large amount in the long run.